India’s RuPay a masterstroke in Financial Inclusion

A Hit or Miss?

Author:– Rugved Mahamuni

Keywords:- RuPay, India, Economy, NPCI, UPI, Payment, Domestic, PMJDY, Financial Inclusion, VISA, MasterCard

ABSTRACT

RuPay is India’s financial master plan for the inclusion of the unbanked population to provide them with banking facilities so that they can support the Indian economy by doing their bit. RuPay gives the government a pipeline to distribute schemes and services to the people of India, India can and is providing facilities to those segments of the population which will otherwise never be catered to by other companies like VISA and MasterCard. Also, it filled the need for a domestic financial transactional system. RuPay was sophisticatedly planned by the National Payments Corporation of India (NCPI) to show the world that India can produce its payment system and not be entirely dependent on foreign payment systems.

RuPay was launched to fulfil RBI’s aim to offer an indigenous a multilateral. Open-loop system which will allow all Indian banks and financial institutions in India to take part in electronic payments and to make India a “cashless society”. Thus, RuPay broke the behemoth duopoly of VISA and MasterCard payment systems by becoming a major player in the financial payments market. RuPay was India’s plan to protect the financial data of its citizens and not allow foreign entities to capture its financial information.

INTRODUCTION

Economics is a major branch of the Humanities and it is one of the most influential subjects which influences human behaviour. Nowadays a new branch has been developed which has a very keen relation to human behaviour and human welfare i.e. Law and Economics. It is not only a subject but also a framework for society to study the pattern of society and provide solutions and remedial measures not only to curb economic problems but also crimes related to economic issues.

Law and Economics are individual subjects but with changing trends in economics and legal structure, it has become necessary to understand the relationship between law and economics. Economics influences law, in the same way, law, influences Economics.

The definition given by Prof. Barker helps us to further understand the relationship between law and economics –

“If economic factors and interests have partly determined the legal framework, it is even more true that law has furnished the whole general framework of rules within which and under which the factors and interests of economics have to work.”[1]

The economic factor which made the government draft a legal framework for improving financial inclusion in India. It was the implementation of the interrelation between law as well as economics in the form of Pradhan Mantri Jan Dhan Yoana (PMJDY).

To analyze this subject it is very necessary to understand the current situation of the Economy concerning boosting financial inclusion on basis of law.

The government of India revolutionized the Indian payment system with the launch of the Pradhan Mantri Jan Dhan Yojana. Thus, giving rise to an iconic venture by the NCPI, we are talking about India’s card network the RuPay card payment system.

Historical Background

NPCI created RuPay as one of its ventures. With the help of relevant provisions under the Payment and Settlement Systems Act, of 2007. It gave way to RBI as well as Indian Banks Association created an online and secure settlement and payment system created domestically in India. Therefore, this initiative of NPCI is included under the “Not for Profit Company” under Section 25 of the Companies Act, 1956.[2]

International Scenario

RuPay was created with the vision to provide the unbanked population with banking facilities and bring about financial inclusion. Such that they can contribute to India’s struggle to become a 5 trillion-dollar economy. Further, the secondary objective was to create an indigenous card payment system to give domestic alternatives to foreign payment services of VISA and MasterCard.

Structure of the Study

Firstly, we look at the payments in India before the entry of RuPay.

Secondly, we observe the master plan of India to introduce RuPay and its effect on the payments market.

Thirdly, we look at how RuPay broke the duopoly of VISA and MasterCard through its wise and brilliantly sophisticated planning.

Fourthly, we analyze the impact of RuPay on weaker and marginalized sections of society.

NATIONAL PAYMENT CORPORATION OF INDIA (NPCI)

NPCI is an umbrella institution for overseeing retail payment systems, it was envisioned by the RBI after setting up the Payment and Settlement Systems board in 2005. NCPI has the core objective of consolidating and integrating numerous systems of varying service levels as well as transforming them into a standard uniform system for retail card payment. The main objective of NPCI is to function in a way beneficial to all of its member banks and the common man at large.

Why was RuPay needed?

RBI’s vision document 2009-12 emphasized the importance of a domestic payment card system and a POS switch network, the two major concerns being –

- Indian banks had to bear the costs affiliated with the association with international card systems due to the absence of a domestic card payment system.

- Most (around 90%) of the transactions from cards were routed using a switch located outside the country.

Due to the absence of a domestic card system, the banks had no other option but to partner with VISA and MasterCard. All the transactions involving these foreign card systems incurred some charges which went into the pocket of VISA and MasterCard.

The estimated charges were around Rs 500 crore every year for the processing of debit and credit card transactions.[4] RuPay is the 7th card payment system in the world after VISA, MasterCard, Amex, Discover, Diner Club, and JCB.[5] The word RuPay was termed after Rupees and payment.[6]

In the speech about dedicating RuPay to the nation, President Pranab Mukherjee stated that –

“An indigenous system like RuPay will, hopefully, not only reduce the dependence on cash and cheque modes of settlement but will also make it easier to offer products based on specific requirements of diverse user sets within the country,” he said while adding that India is one of the few countries in the world to meet domestically the need for card payment system.”

As of 2022, the Currency in circulation is around 14% of the GDP of India[7], which can be considered quite high. To tackle this problem and increase the cashless transactions around India, RuPay is playing a vital role.

BREAKING THE DUOPOLY OF VISA AND MASTERCARD

Before the entry of RuPay, VISA and MasterCard had a dominating stake in the Indian card network market and had established a stable duopoly. But since the inception of RuPay, it has been campaigned and promoted strongly by the Indian Government.

Finance Minister Nirmala Sitaraman while addressing the 73rd annual general meeting of the Indian Banks Association. It asked banks to “only promote RuPay Cards” and ensure that National Payments Corporation of India (NPCI) becomes a brand India product. She further also asked the banks to discourage non-digital payments.[8]

To improve the reachability of RuPay the Indian Government announced the incentive scheme for RuPay and BHIM-UPI. Though, this scheme the government will incentivise the acquiring banks by paying a percentage value of the transactions processed through RuPay and BHIM-UPI. Rs 1300 crore will be spent on this scheme for the FY 2021-2022. To further develop the RuPay payment system India will be reimbursing the Merchant Discount Rate (MDR) in the P2M (person to merchant) transactions. Union Minister Ashwini Vaishnaw stated that the incentive shall be viewed as an investment for digital payments. The government with this scheme expects people to adopt digital payments and go cashless.[9]

What Is MDR and How Did It Affect the Duopoly?

India has come a long way when it comes to digital payments. We can say so because one can buy everything from cement to groceries from a store even if you don’t have physical cash with you. However, a lot is going on behind a transaction.

Important party for executing a transaction

- Issuer Bank

It is the bank in which the cardholder has his/her account.

- Acquirer Bank

It is the bank which has acquired the transaction or the bank whose POS terminal has been used is the Acquirer Bank.

- POS (Point of Sale)

The transaction between a merchant and a customer is when a service or product is purchased using a “Point of Sale” system for completing the transaction.

Type of Fee Levied

There are 4 types of fee levied in a transaction as follow:-

1. MDR (Merchant Discount Rate)

Did you know that each time you make a transaction using a card. The merchant gets charged a percentage of the transaction amount, this percentage is called as Merchant Discount Rate (MDR). MDR is typically between the range of 1-3% of the overall amount. Let’s take an illustration for understanding the following concept –

If you buy product Rs.1000 and make payment using a card then the merchant has to pay MDR of Rs.X on it.

2. Switching Fee

After UPI, cards are the second most preferred method of digital payment. If you have used a debit or credit card for payment you will know that each card is issued by an institution (RuPay, VISA, MasterCard, AMEX), and they levy a processing fee to the card’s issuing bank. This processing fee is called the Switching Fee. It is also known as the routing transaction fee.

The switching fee varies from 0.15% to 1.00%.

3. Interchange Fee

When you swipe a debit or credit card the funds are transferred from the issuing bank to the acquiring bank and RuPay and other institutions facilitate the transfer process. The issuing bank makes its share of the profit by charging the interchange fee.

The issuing bank charges the acquiring bank a percentage of the transaction plus a fixed amount.

Thus, the average interchange fee is around 1.81% for credit cards and 0.3% for debit cards.

4. Payment Service Provider Fee (PSP)

To understand the Payment Service Provider fee, let’s first understand PSP.

A payment service Provider is a SaaS (Software as a Service) based enabler, it acts as an aggregator between the merchant and the customer.

To put it simply PSP helps businesses to accept online payments via multiple modes like UPI, real-time bank transfers, as well as debit and credit cards.

PSP fee is the processing fee that PSPs charge to take care of all the required needs. PSPs might have a fixed model while others might have a variable model for charging a fee. Some PSPs charge a set-up fee and annual maintenance charges.

Examples of PSP – RazorPay, PayPal, JusPay, Instamojo etc.

NPCI was set up by RBI to develop homegrown payment and settlement systems in India. With NPCI being a not-for-profit company it automatically becomes a way forward to financial inclusion using subsidised services.

The government has been supporting RuPay usage since its inception, the government has emphasized the equivalence of using RuPay to nationalism and supporting the Indian economy.

Better Cost Efficiency of RuPay –

The government introduced regulations under which RuPay payments would come under the Zero-MDR norm[10]. Also, no charges will be levied from the merchants for transactions using the RuPay cards. Further, the operating costs for using RuPay are lower as compared to VISA and MasterCard. Banks using VISA and MasterCard are charged a quarterly fee for using their network. As RuPay is a domestically grown network banks do not need to pay any extra charges.

A part of the effect of Zero MDR can be analysed by accessing the status of RuPay debit cards by comparing the year-on-year growth of PMJDY accounts opened and the cards issued to these accounts.

Figure 1 – Data from RBI and DFS

The black line near September 2019 represents the introduction of Zero MDR regulations of the RBI for RuPay. We can see that the y-o-y growth of PMJDY accounts was consistent though there was a decline in the y-o-y growth of RuPay debit cards. While there was a decrease in RuPay debit cards there was an increase in the overall issuing of debit cards, which implicitly reflected to increase in VISA and MasterCard debit cards.

MasterCard’s Non-compliance with RBI directives –

RBI barred MasterCard from issuing any new cards through notification with effect from July 22, 2021. MasterCard was found to be non-compliant with the provisions laid down by RBI for the Storage of Payment System Data. It directed system providers to ensure that all payment system-related data must be stored in India. Therefore, it was directly advantageous to RuPay and VISA many banks were forced to move to RuPay and VISA cards.[11]

RuPay was successful in capturing a 60% share of the Indian card market in 2020, this is much higher when compared to RuPay’s 15% share in 2017. It has shown exponential growth and still has untapped potential as the number of cards issued by RuPay is still small as compared to its international rivals VISA and MasterCard. RuPay also lacks in volume and the average value of transactions in the card market.[12]

FINANCIAL INCLUSION

PMJDY was an ambitious scheme launched by India with the main objective of financial inclusion. This scheme was introduced in 2014 by PM Narendra Modi.

PMJDY ensured access to a basic saving bank account, access to basic credit, insurance and pension schemes and remittance facilities to the ignored sections of society, i.e. Lower income groups, and weaker sections.

The objectives of the scheme were as follow –

- To ensure access to financial services as well as products at an affordable price.

- Using technology to reduce costs, thus widening the reach of financial tools.

The PMJDY plans to channel all central/state as well as local benefits directly to the beneficiary’s bank accounts and push the Union government’s Direct Benefits Transfer (DBT) scheme.

Each new account was provided with a RuPay-linked debit card[13], also RuPay was introduced as a domestic alternative to foreign payment systems giants.

The behemoth payment processors such as VISA and MasterCard had a duopoly in the Indian card payment market, dealing with billions of credit and debit transactions daily. They wielded too much power and authority even beyond the imagination of the government itself. Also since the majority portion of payment systems was under the control of private players they had little to no interest in the welfare of the Indian consumers.

PMJDY Role

Though in the 2010s only 1/3rd of the population had a bank account, that too with minimum balance requirement. This caused the marginalized to be left out from accessing banking facilities.[14]

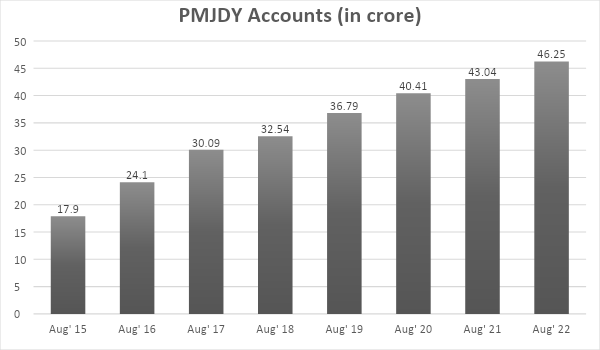

To counter this the PMJDY was launched through which zero-balanced accounts with overdraft facilities as well as deposit insurance were offered to the financially excluded population. Because of which the number rose to a staggering 46.25 crore accounts by 2022. Out of which 25.71 crore (55.59%) account holders were women and 30.89 crores (66.79%) accounts are in semi-urban as well as rural areas.[15]

Figure 2 – Data from – rbi.org.in

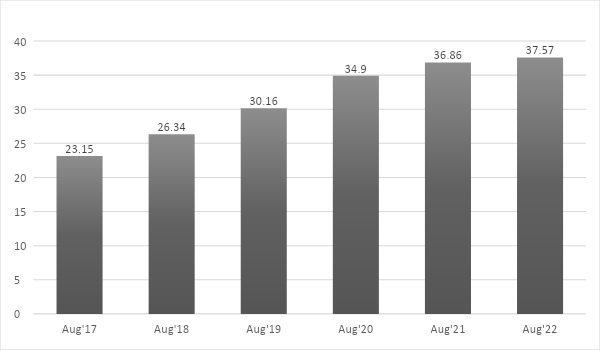

Though the RBI guidelines, a PMJDY account is considered inactive if no customer-related transactions are induced in the account for over 2 years. As of August 2022, 81.2% of PMJDY accounts were operative and only 8.2% of PMJDY accounts were zero balance accounts.

Figure 3 – Data from – rbi.org.in

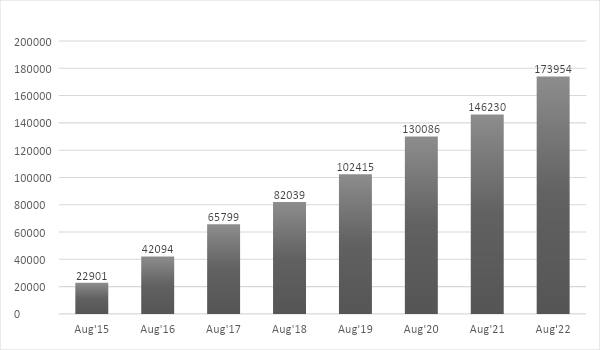

As of 10th September 2022, the total amount of money in PMJDY is around Rs 1,73,954 crore.[16]

Figure 4 – Data from – rbi.org.in

Total deposits in PMJDY accounts have increased by 7.60 and accounts have increased by 2.58 times from August 2015 to August 2022.

RUPAY’S ROLE

All the accounts opened under PMJDY were provided with cards linked to RuPay. RuPay set a record by issuing 1.81 crore new accounts in less than a week.

RuPay is well poised to support banks’ issuance of debit and prepaid credit cards, with the primary objective to increase retail electronic payments in India. It further launched virtual cards (June 2016), contactless cards (June 2016), and Credit cards (June 2017).[17]

RuPay had already laid out a roadmap

RuPay wanted to give tough competition to the international players in the payment market so RuPay customized its experience in such a way it was sophisticatedly made for Indian consumers, following are the differences between RuPay and other cards –

| Point of difference | RuPay | VISA & MasterCard |

| Cost of transaction | Transaction costs are lower for domestic clearing and settlement | Transaction costs are higher due to the international settlement process |

| Data Storage | All financial transactional data of customers remain within India | All financial transactional data of customers is processed outside of India |

| Integration Costs | No quarterly fee or entry fee is charged to Banks | Quarterly fee and entry fee has to be paid by Banks |

| International Acceptance | Currently doesn’t support international transactions within India | All domestic and International transactions accepted |

| Supported Card Types | Supports both debit and credit cards | Supports both debit and credit cards |

RuPay Launched 5 Types Of cards with the Intention Of Financial Inclusion

1. RUPAY PMJDY DEBIT CARD –

This card is issued to the account holder of PMJDY, this card allows the cardholder to make transactions at all ATMs, POS terminals, as well as e-commerce websites. Also, this card comes with a personal accidental death and total disability insurance of two lakh rupees.

2. RUPAY MUDRA DEBIT CARD –

Under PMJDY, all beneficiaries under the Mudra loans are eligible for the RuPay Mudra debit card. The objective of the Mudra card is to avail working capital facility as a cash credit arrangement to the account holder and to support the micro-enterprise sector to grow.

With this card, one can make multiple withdrawals and avail credit for managing the working capital limit efficiently and productively. Thus, it helps the micro-enterprise by reducing the interest payment burden. The cardholders are also eligible for merchant offers at the time of purchase.

3. RUPAY PUNGRAIN DEBIT CARD

PunGrain is a project developed by the Punjab government in October 2012 for grain procurement, to help farmers across Punjab.

Also, PunGrain cards can be used at all ATMs, POS, and e-commerce websites. But the main purpose of this card is to avail automatic grain procurement facilities at the PunGrain mandis.

4. RUPAY KISAN CREDIT CARD

All farmers having an account under the Kisan credit card scheme are provided with Kisan Credit Card. This initiative was the undertaking of the Ministry of Agriculture to provide credit support to the agricultural sector. Also, the card was provided for all cultivation needs and non-agricultural needs in a cost-effective manner.

This card can be used at all ATMs, POS, as well as e-commerce websites.

5. MSME RUPAY CREDIT CARDS

This credit card provides the following services –

- Personal Accidental Coverage of Rs 10 lakhs

- Air accident Insurance of Rs 20 lakh as well as

- Also, Baggage loss Coverage of Rs 20,000

- 24*7 Concierge Services, and

- RuPays Focus

While the function of RuPay is to create facilities for funding the unfunded, keeping in mind the needs of the rural public. It also focuses to improve the overall banking services and positioning itself as a reliable, premium brand in the payment card market.

In accordance to achieve this objective NPCI has partnered with Discover Financial Services as well as Diner Club, using this association all RuPay card holders can now utilize the networks of the partnered entities for international transactions and to access cash outside India.

RuPay Platinum is such an initiative for attracting higher-end customers in the country. This card offers value-added benefits such as insurance, complimentary airport lounge access, and cashback on utility bills. RuPay further has partnered with Japan’s JCB International and Union Pay of China.

Findings

RuPays success in driving financial inclusion among the masses remains a debatable issue as the activity rates of RuPay cards remain low. Also, RuPay makes up a small portion of transactions in the market as compared to VISA and MasterCard.

RuPay was launched with the aim of Financial Inclusion and it specifically targeted people from semi-urban and rural areas. We can say that it was successful in reaching the remotest parts of the country.

Impact of RuPay cards on marginalized sections of society

As per a report made by the National Bank for Agriculture and Rural Development (NABARD) analyzing the effect of RuPay on weaker sections of Bihar and Uttar Pradesh,

In Bihar –

- It was found that 96% of RuPay cards were issued to economically weak communities. While the rest 4% to people from the general category, but the illiteracy of the cardholders is the major drawback. That is affecting the ability of the cardholder to utilize the benefits under PMJDY and the RuPay card. 46% of the cardholders were illiterate or had studied till the primary level.

- 57% of the cardholders were women, who mostly were non-working housewives. Although, irrespective of the above fact women are making financial decisions and withdrawing money from the account and operating the account on an occasional basis.

- As PMJDY has digital banking facilities the young group of the weaker and marginalized communities view a behavioural change at an early age.

- 87% of the cardholders now feel the bank services are closer to them.

- Out of 1315 cardholders, 57% use RuPay cards now instead of cash transactions.

- 49% of the cardholders reported that they started saving money in their bank account.

- Also, 85% of the PMJDY account holders have the RuPay debit card, out of the 85% of account holders 60% of cardholders use the RuPay Debit Card.

- 71% of the cardholders who availed of the overdraft facility, felt that the facility was useful.

In Uttar Pradesh,

- It was found that 76% of RuPay cards were issued to economically weak communities and the rest 24% of cards were issued to people from the general category.

- Around 40% of the cardholders were illiterate or had studied till the primary level.

- 63% of the cardholder now use RuPay cards instead of cash transactions.

- 66% of the cardholders started saving money in their PMJDY accounts.

- 72% of active cardholders who use RuPay cards feel that it saves time and transportation costs.

- Around 31% of the RuPay cardholders are aware of its financial benefits or economical benefits.

- 79% of the cardholders can use the card independently.

- Also, 94% of the cardholders who availed of the overdraft facility felt it was useful.

Overall, we can state that RuPay was able to bring financial literacy to some extent to the cardholders in Rural areas, such that they understand the financial benefits of the RuPay card and its digital facilities. This in turn has exponentially increased financial inclusion in the rural areas of India, as stated in the report made by NABARD. RuPay was somewhat successful in making banking facilities available to the unbanked population of the rural areas.

CONCLUSION

1. RuPay – superhit stroke of India:

RuPay overcomes a super hit stroke of India as it has managed to capture a 60% share of India’s card market in 2020 as per data released by the Reserve Bank of India. Till now 628.41 million RuPay cards had been issued across all categories including prepaid, debit, credit and commercial cards. “RuPaye has surpassed visa as the largest payment card network in India”, says the NPCI. During the Covid-19 pandemic, consumer usage of the RuPay platform was hovering at 87% to 98% which was above its foreign competitors MasterCard and Visa which were at 70% and 86%.

2. PMJDY – Road to RuPay’s victory:

RuPay cards got a major boost through Pradhan Mantri Jan Dhan Yojana through which they were issued to Jan Dhan account holders. As of 10 March 2021, a total of 308.5 million RuPay debit cards had been issued to Canadian account holders.

3. RuPay- helps with insurance for its cardholders:

The risk coverage under the Pradhanmantri Suraksha Bima Yojana given by RuPay is Rs. 2lakh for accidental death and full disability and Rs. 1lakh for partial disability. The premium of Rs.20 is to be deducted from the account holder’s bank account through the auto debit facility in one instalment.

4. RuPay – Trouble resolver for MSMEs:

Also, RuPay has launched MSME RuPay credit cards to facilitate simplified payment mechanisms to give MSMEs the to meet their business-related operational expenses. The card is being offered in Association with the National Payments Corporation of India.

The benefits offered by the RuPay card are anytime digital payment, an interest-free period and will carry an interest rate similar to the rate charged for loans.

MSME borrowers will be able to enjoy an interest-free credit period of up to 50 days on their business spending. MSME Will also get specially curated efficient business services which will help them to take their business on most of the digital platforms. The RuPay card will simplify and expedite the payment mechanisms for MSMEs while enabling banks to monitor transactions at a granular level.

5. RuPay – Saviour of financial data:

RuPay to great extent had saved financial data from being disclosed to other countries. As the behemoth duopoly of VISA & MasterCard has been broken, the financial data of India is much safer. Foreign cardholder companies had lost their total access to transactional information due to RuPay.

6. RuPay- trying to make its monopoly:

With the support of the Indian Government and politicians. RuPay is trying to be a monopolist in the Indian payment market, flaunting the line between healthy and unhealthy competition.

Addressing this issue, VISA has complained to the US government that the Indian government supporting RuPay is damaging VISA’s potential in the country. Although the complaint didn’t bring in a fruitful result.

Also, all Indian companies with an annual turnover exceeding Rs. 50 crore are required to offer RuPay payment options to their customers which states the monopoly of RuPay.

Moving toward universal financial inclusion has been a policy priority for the Reserve Bank over the last few years. Since financial inclusion becomes a critical financial component for ensuring sustainable and equitable economic growth to achieve this goal India has to focus on improving the digital infrastructure of India.

7. Law – The Backbone of RuPay

Rupay was introduced due to the changes in the provision of the Payment and Settlements Act, 2007. This was the move of India to tackle financial issues through law. The aim for which Rupay was launched could be achieved with the help of Law because, the law is the foundation of a good economy, and vice versa.

Recommendations

1. Global acceptance:

To improve its performance and increase its profits, RuPay should jump into a global market with its transaction facility, making RuPay an internationally accepted payment system. In September 2019, the RuPay Select card was made available in Dubai for international payments, as well as the RuPay JCB Global card was launched in July 2019. This card was made in partnership with the Japanese JCB Global card payment network.[18]

2. RuPay should make recurring payments more accessible to the cardholders –

RuPay 2.0 was recently launched which allows recurring payments. But cardholders aren’t much aware of the launch, RuPay should invest in improving the financial literacy of their customers. Also Rupay can tap into the untapped market for recurring payments. This would increase the consumer base using RuPay cards and gradually it will increase the revenue of RuPay.[19]

3. RuPay should increase the issuance of Rupay cards –

As shown in Fig 1, after the implementation of the Zero MDR policy the issuance of RuPay cards was reduced. VISA as well as MasterCard took advantage of this and increased their issuance of cards. If Rupay increased the issuance of cards it would tap into the untapped portion of the population which has yet not experienced digital payments through cards.

4. National Payments Corporation of India (NPCI) should scrap the ZERO merchant discount rate (MDR) policy –

Due to the presence of ZERO MDR government of India has to subsidise MDR in RuPay transactions which causes RuPay to suffer from losses. If the subsidization of MDR in RuPay transactions is prohibited the money used for subsidizing can be used in other public policies. A few serious questions arise in front of the government: What other sources of money to subsidise MDR if the present amount is fully utilised? Also, can continuous subsidization of MDR may create a heavy burden on the Indian Economy

References

- Dr George Barker, Australian National University, https://researchers.anu.edu.au/researchers/barker-g

- RuPay, Securing a dream of cashless India, https://www.RuPay.co.in/about-us

- RuPay – Product booklet, National Payments Corporation of India (NPCI), https://www.npci.org.in/PDF/npci/RuPay/Product-Booklet.pdf

- NDTV, Finally India card RuPay to replace Visa, Mastercard, October 29 2011, https://www.ndtv.com/business/finally-india-card-RuPay-to-replace-visa-mastercard-2674

- Economic Times, RuPay, India’s payment gateway, launched, on 4th May 2014, https://economictimes.indiatimes.com/wealth/personal-finance-news/RuPay-indias-own-payment-gateway-launched/articleshow/34845083.cms

- Supra Note 1

- Reserve bank of India, Annual report, Currency Management 2022, https://m.rbi.org.in/scripts/AnnualReportPublications.aspx?Id=1350#:~:text=Currency%20in%20Circulation-,VIII.,10%20and%20%E2%82%B920%20denominations

- Indian Banks Association (IBA), 73rd Annual General Meeting, 10th November 2020 at 3:00 p.m. https://www.iba.org.in/circulars/indian-banks-association-iba-is-organizing-its-73rd-annual-general-meeting-on-november-10-2020-at-3-00-p-m-through-e-platform-_992.html

- Ministry of Electronics and Information Technology, Notification, Incentive scheme for promotion of RuPay Debit cards and low-value BHIM-UPI transactions (P2M), 17th December 2021, https://egazette.nic.in/WriteReadData/2021/231960.pdf

- Id.

- Reserve Bank of India (RBI), Press Release, Reserve Bank of India takes supervisory action on Mastercard Asia / Pacific Pte. Ltd., Jul 14, 2021 https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=51895

- Reserve Bank of India (RBI), Reports, Benchmarking India’s Payment Systems, https://m.rbi.org.in/scripts/PublicationReportDetails.aspx?UrlPage=&ID=923

- Supra Note 2

- Reserve Bank of India (RBI), Annual Report, Credit Delivery and Financial Inclusion, https://rbi.org.in/scripts/AnnualReportPublications.aspx?Id=1001

- Ministry of Finance, Press Release, PMJDY – National Mission for Financial Inclusion, completes eight years of successful implementation. https://pib.gov.in/PressReleasePage.aspx?PRID=1854909#:~:text=PMJDY%20Accounts%20have%20grown%20three,for%20the%20Financial%20Inclusion%20Programme.

- Id.

- RuPay, RuPay Milestones, https://www.RuPay.co.in/milestones

- Id.

- RuPay, Introducing RuPay 2.0, https://www.rupay.co.in/rupay-advantage

Mail us at edumoundofficial@gmail.com